A Glimpse of Frontier Macroeconomics

Why Macroeconomics isn’t just about growth and business cycles anymore

If a central bank raises interest rates, inflation should fall. That is the “common-sense” story most of us learn the first time. Then you hear John Cochrane say something that sounds upside down: “higher interest rates means higher inflation.”. Wait — How is that possible? Under what conditions?

This is the moment of realization that macroeconomics is not just a list of slogans, but a discipline about mechanisms — about how outcomes are produced, and how those outcomes depend on institutions, expectations, constraints, and assumptions.

And even when the policy and its mechanism “works”, the bigger question we should be asking is: Inflation on what? Inflation for whom? or even better, who wins and who loses? The rich? The poor? People living paycheck to paycheck? People who barely even know what an interest rate is, but still feel its effects every month? These are not side questions. They go straight to the heart of how the economy works. This is where frontier macroeconomics begins.

Let’s take a step back and understand what do we really mean by macroeconomics. At its core, macroeconomics is a study of the performance of the national and global economies. Traditionally, the two headline questions were growth and cycles: why living standards rise in the long run, and why economies boom and slump in the short run.

But the modern version of macro doesn’t stop there. It asks: growth for whom? cycles for whom? That shift happened for a practical reason. When real economies went through episodes like jobless recoveries after the 2008 global financial crisis, decentralization reforms that shifted fiscal responsibilities, and the massive income shocks like the COVID-19 pandemic, it became harder to pretend that the “average household” is the whole economy. The distribution of income, wealth, and risk shapes how policies transmit through the economy — and ultimately, whether they work at all. Inequality has therefore become an increasingly central theme of modern macroeconomics.

Frontier macroeconomics starts with its bottom-up approach: microfoundations. Instead of treating the economy as a single machine moved by a few aggregate relationships, modern macro asks a more disciplined question: what decisions are households, firms, banks, and governments actually making, and how do those decisions add up to aggregate outcomes?

A useful place to begin is the Solow–Swan model1, the classic in growth theory. It is powerful, but deliberately simple. Many of its key drivers are treated as given — or, in economic terms, exogenous. In its standard form, the model starts with a production function in which aggregate output (Y) is produced using capital and labor.

The backbone of the model is capital accumulation: not all output is consumed today, and the portion that is saved is reinvested to build the capital stock for the future. This process is what drives growth over time. A simple way to think about it is “saving an egg today so you can have more chickens tomorrow.”

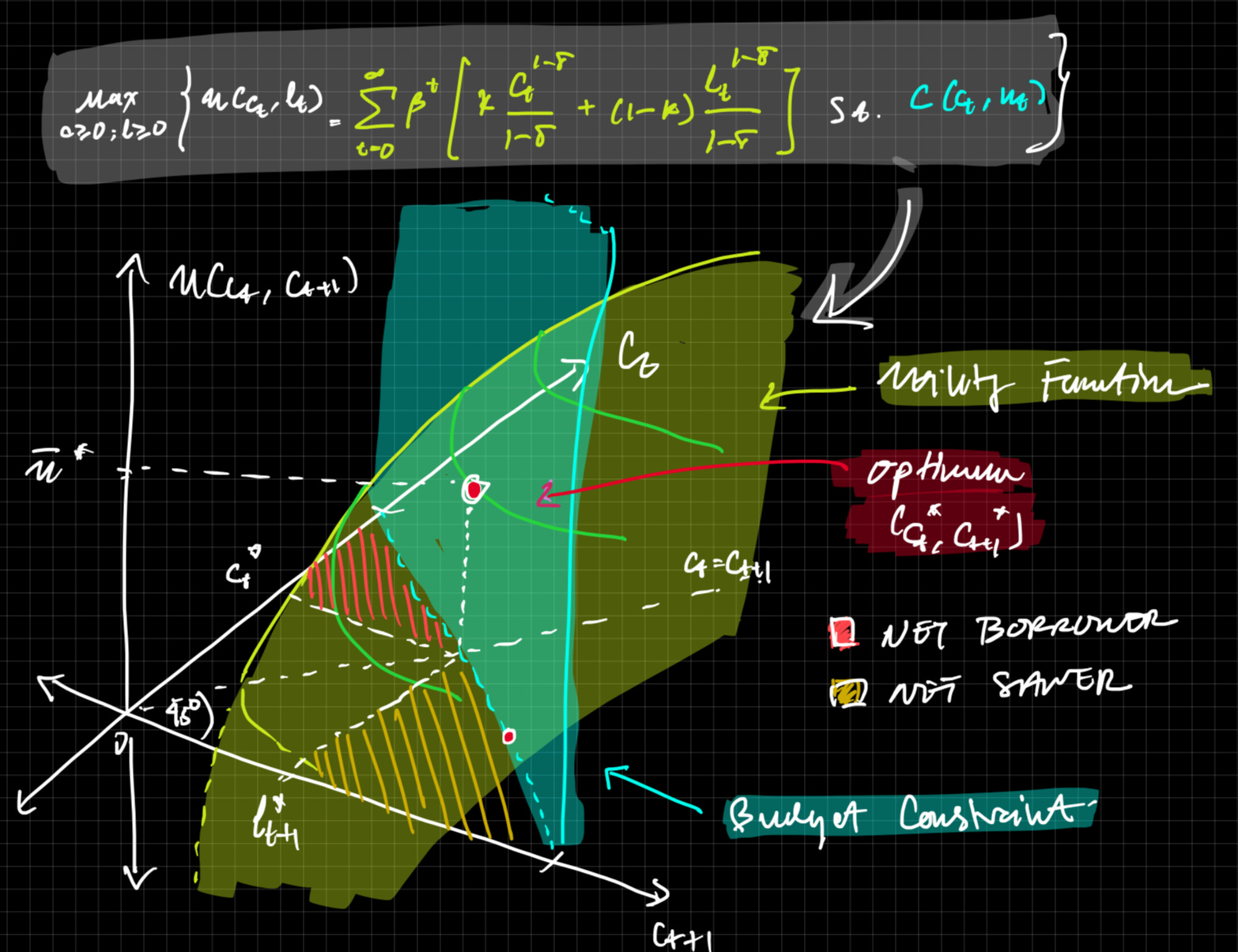

One of the most important elements in the Solow model is the saving rate. The model assumes households save a fixed fraction of income. That simplicity is useful, but it also leaves an important question unanswered: why do households save that amount in the first place?

Modern macroeconomics pushes directly on that gap. Instead of taking saving as given, microfoundations ask: how does saving emerge from household decisions? How do people choose between consuming today and saving for tomorrow? Since households do not simply spend everything at once, theorists model that trade-off explicitly through an intertemporal utility maximization problem. In other words, saving is no longer imposed from outside the model; it becomes the result of optimization.

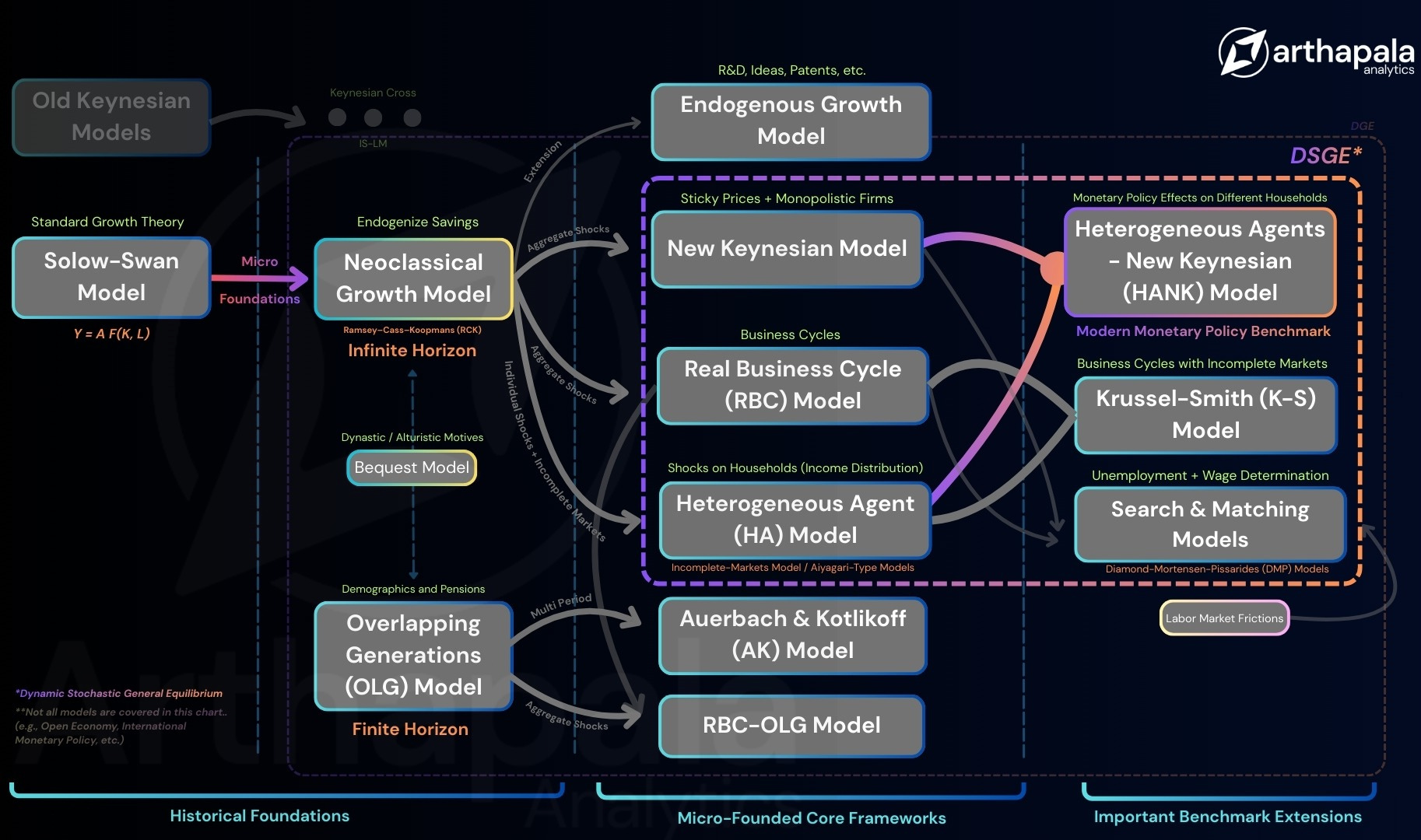

These optimization behavior of not only households, but also firms, governments, and other agents marks the transition from older growth models to the broader architecture of modern macro. The diagram below gives a broad roadmap of how these models evolve and connect to the benchmark frameworks used in modern macroeconomics. What follows is a quick tour of some of the most important ones.

Neoclassical Growth Model (NGM) / Ramsey-Cass-Koopmans234

This is the classic micro-founded growth model. It explains how households choose consumption and saving over time, and how those choices shape capital accumulation and long-run growth. It is used as the foundational benchmark for modern dynamic macro models.

Overlapping Generations (OLG) Models56

People do not live forever. The OLG model introduces finite lives: people are born, work, save, retire, and die. It is designed to study how different generations interact. It is especially useful for analyzing pensions, aging populations, public debt, social security, and intergenerational redistribution.

New Keynesian (NK) Model7

Prices do not adjust flexibly. The New Keynesian model takes the dynamic structure of modern macro and adds sticky prices, nominal rigidities, and imperfect competition. Its main purpose is to explain why monetary policy has real effects in the short run. It is widely used to study inflation, interest rates, business cycles, and stabilization policy.

Heterogeneous-Agent (HA) Model89

The HA model drops the idea that everyone in the economy is basically the same. Instead, households differ in income, wealth, risk exposure, and constraints. These models are used to study how inequality, incomplete markets, and household-level shocks shape aggregate outcomes.

Heterogeneous-Agent New Keynesian (HANK) Model10

HANK combines heterogeneous households with a New Keynesian monetary framework. Its main contribution is showing that monetary policy does not affect all households in the same way. It is increasingly used as a modern benchmark for monetary policy analysis, especially in central banks, because it captures distributional effects and more realistic transmission channels.

Search and Matching Models111213

This models focus on labor market frictions. Workers do not instantly find jobs, and firms do not instantly find suitable workers. These models are used to explain unemployment, vacancies, wage bargaining, job creation, and labor market dynamics.

One application of the OLG models is the study of pension reform in Indonesia. Kudrna, Piggott, and Poonpolkul (2022)14 show that extending pensions can raise welfare, especially for older informal workers, but also creates long-run fiscal trade-offs as the population ages. This shows how policy affects different generations and fiscal sustainability over time.

In essence, frontier macroeconomics is not a rejection of traditional macroeconomics. It is when the old questions are taken more seriously. Growth still matters. Business cycles still matter. But modern macro asks those questions with sharper tools: by making behavior explicit, by taking frictions seriously, and by recognizing that households and firms are not all the same. The field has evolved from simple aggregate relationships towards models built upon optimization (why households choose to consume, save, or work), expectations (what do people believe about inflation, wages, or policy tomorrow), and constraints (how firms finance investments, how household borrow, and where markets fail).

This matters most when the economy is hit by shocks or policy changes. A tax reform does not affect capital owners and workers in the same way. An interest rate hike does not hit rich households, indebted households, and hand-to-mouth households equally. A recession is not just a fall in output; it is also a change in hiring, job finding, and household risk. Frontier macroeconomics matters because it gives us a way to study those mechanisms directly, rather than hiding them behind one “average” household.

That said, frontier macroeconomics still faces important critiques. Even sophisticated models depend heavily on assumptions, and microfoundations do not automatically make them true. Expectations may be modeled too neatly, data are often hard to identify cleanly, and policy conclusions can change depending on which frictions the model emphasizes. In light of this, frontier macro should not be seen as a one-fits-all framework. Rather, macroeconomic models are useful precisely because they help isolate specific mechanisms and clarify what drives economic outcomes in different contexts. As Dani Rodrik puts it in Economic Rules: “The correct answer to almost any question in economics is: It depends.”