Incomplete by Design: How Growth Theory and Measurement Evolve

How History Reveals the Incompleteness of Growth Models and Definitions

The history of economic growth has been shaped, in large part, by the process of defining what growth is and what it is not. The evolution of how growth is understood has been created by sequences of economic thought and theoretical foundations. Each sequence does not replace what came before, but reveals what the previous framework could not see. Acting as an iterative discipline, each framework will shape a new foundation, producing a chain of succession rather than replacement.

This iterative process was often ignited during a crisis, such as one shown during the Great Depression. In the worsening condition, policymakers were puzzled to find a reliable metric of its economic impacts. It was during this period that Simon Kuznets, a Russian-American economist and statistician, contributed to the creation and formalization of Gross National Product (GNP). It was defined as the total value of output by a nation’s population, regardless of location. His framework later provided the foundation for Gross Domestic Product (GDP), measured as the sum of consumption, government expenditure, investment, and net exports. Adopted as an international standard for economic performance, it has become the primary lens for economic measurement (Vanham 2021).

Yet, the establishment of GDP as an international metric did not come without challenges. Kuznets himself argued that using GDP as a measure of national welfare will overlook other aspects, including the quality of life, environmental degradation, and income inequality. Therefore, despite providing a foundation for GDP, he expressed a profound disagreement with simplifying the overall definition of economic performance as a measure of productive output (Vanham 2021).

This tension illustrates that a metric could be utilized with numerous interpretations. While GDP provides a consensus, Kuznets showcased that a singular definition of growth should be challenged. More importantly, disagreement regarding definitions should be taken as a corrective process to enhance our understanding of economic progress.

Such a sequence illustrates a recurring pattern that ideas, regardless of how well-formed, are constrained by what they can explain at a particular time. History acts as a record that keeps track of ideas and how they were exposed, revised, and advanced. Thus, with the reach contestation, our understanding of how capital, labour, growth, institutions, and technology will be shaped.

After the Great Depression, the idea that “supply creates its own demand”, known as Say’s Law, was rebutted . The world needed a new intellectual axiom, and at the end of the Great Depression, “The General Theory” by John Maynard Keynes, emerged. It argued that instead of wages, employment is decided by the aggregate demand for goods and services. Rebuking the classical theory, he asserts that government intervention is a necessary tool to help the economy reach full employment.

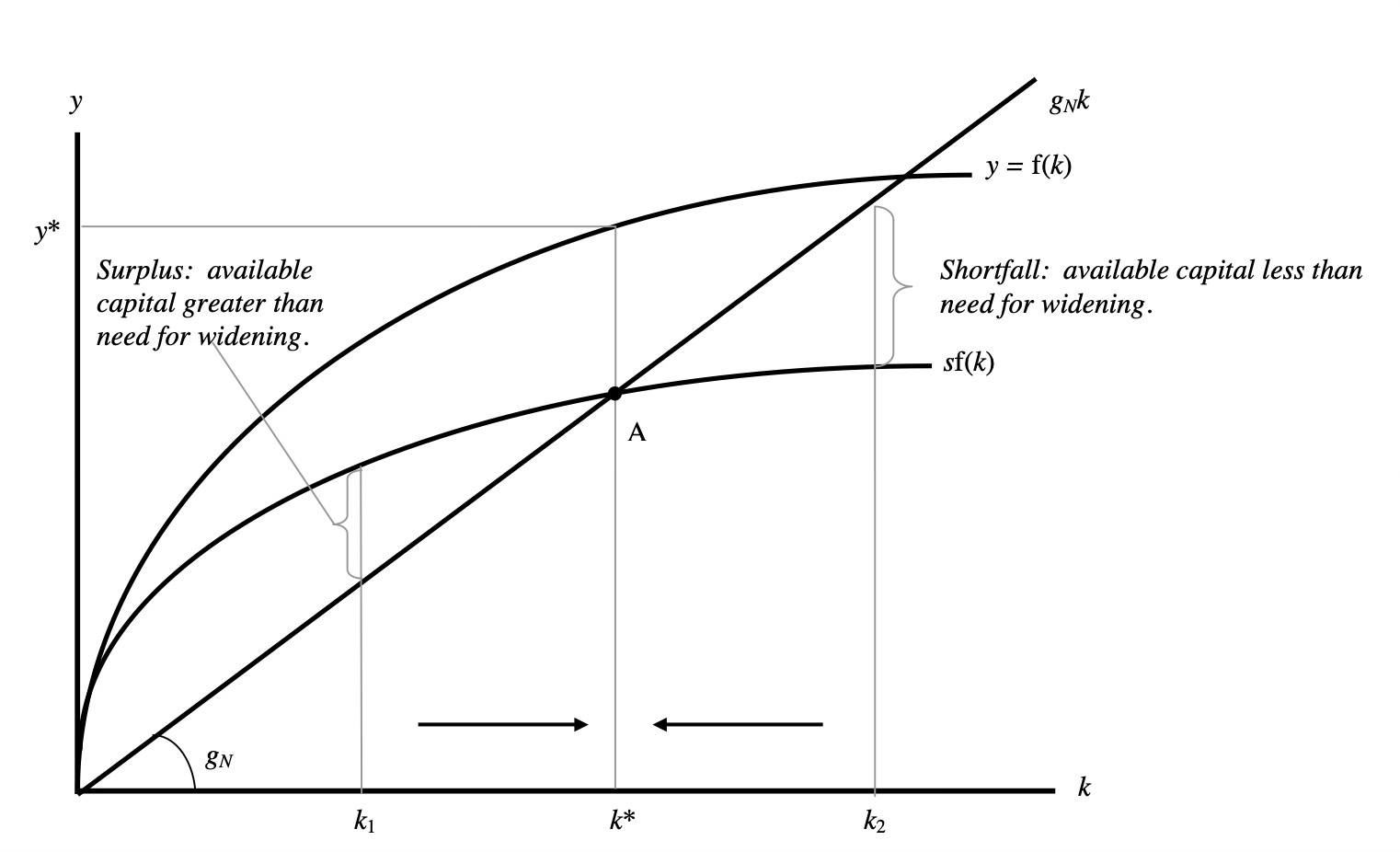

Building on the Keynesian framework, the Harrod-Domar model was one of the earliest to be introduced. It shows that economic growth is strictly a byproduct of the saving rate and the capital-to-output ratio (Boianovsky 2018). The idea became a landmark for capital fundamentalism, emphasizing capital formation as the main driver of economic growth. The model became enormously influential during the late 1940s to the mid-1950s, being one of the first models of the post-war growth theory.

Criticism emerged shortly after its birth. Comments were made highlighting fundamental problems with the model’s assumptions, defined as the knife-edge instability (Hagemann 2009). Particularly, the model assumes that the warranted rate of growth and the natural rate of growth are exogenously given without mechanisms to align them. This assumption produces an extensive period of rising or falling unemployment. In addition, fixed proportions of labour and capital add to the problem, leaving the model fundamentally unsustainable.

In 1956, the Solow-Swan model became a direct response to the Harrod-Domar model by asserting the roles of technological advancement and the substitutability of labour and capital as factors of production (Hagemann 2009). The model empirically proved the idea in 1957 through the “Solow residual”. It illustrates that a large portion of growth cannot be attributed to capital accumulation or population growth, implying the significance of total factor productivity towards income increase. The discovery effectively iterates the notion that capital accumulation is the determining factor of economic growth.

This sequence is not simply an empirical finding or a theoretical advancement, it was an acknowledgement. From a historical standpoint, it validated the claim that definitions of growth and its measurements are rarely final. More importantly, our understanding of growth will only continuously evolve.

The Solow-Swan began by scrutinizing the instability of its predecessors, only to create room for other sources of evaluation. It validated the limitation of capital as a factor of growth, but left the specification of total factor productivity for interpretation. Thus, theoretical evolutions will be limited by our understanding of current phenomena. Each solution will only expand the question, and not conclude it indefinitely.

After dominating growth theory for decades, the Solow-Swan model was eventually displaced by the Endogenous Growth Theory. The new theory improved upon the model, adding human capital and knowledge spillovers to the construct of total factor productivity (Lucas 1988; Romer 1994). Other perspectives, such as the Adaptive Efficiency Model, argues that growth is a byproduct of institutional adaptation, highlighting the conditionalities imposed by evolving institutions on economic growth (North 1994; Simpson et al. 2025).

Together, they define growth as a byproduct of several endogenous factors. They illustrate the limitations of past models as a predictive tool for growth. They did not replace the Solow-Swan model, but our understanding of growth has changed permanently since they emerged.

These models support the claim that defining growth should come as an evolutionary process. The statement that “the economy grows because of fast capital formation” is deceptive in its simplicity and only partially true. Growth is a phenomenon influenced by many factors, and attributing one factor without the other can only produce an incomplete understanding of its nature.

Acknowledging capital formation as a driver of growth is crucial. However, human capital, knowledge, and institutions determine how capital should be accumulated and will be deployed. The Solow-Swan model confirmed the idea that capital and labour can only explain a fraction of growth, and it has proved the limitation of capital accumulation as its primary explanatory factor.

The consequence of misalignment extends beyond theory. The Harrod-Domar model dominated post-war growth discussion, but its failure in creating a sustainable growth mechanism had severe consequences. It undermined alternative growth factors, and overemphasized its own importance and creates a disproportionate burden on developing countries, implying barriers of equitability (King & Levine 1994).

The same goes for the Solow-Swan. After being the primary reference for understanding growth, it failed specify total factor productivity at the empirical level. Without theoretical improvement, technological advancement could only be understood more broadly, significantly limiting understanding of growth factors, and thus, its policy implications.

The past dynamics of GDP and GNP also display a similar conflict. We agreed that growth is measured as an increase in productive output. But such a definition is not final. There will always be room to incorporate other definitions of growth, allowing alternative measurements to take place, and in effect, other models to emerge.

Therefore, the question of defining and measuring economic growth is not a question of empirical specification, but a clash of consensuses. GDP is a construct of economic growth, but not the entirety of it. The same way that capital formation is proven to be only a factor of growth, and not its whole.

Economic growth is not a problem awaiting a final solution, it is a moving object. The progression from Harrod-Domar to Solow to Endogenous Growth Theory is not a story of convergence but a record of succession, for each exposed the blind spots of its predecessor. Disagreement about definition and measurement is therefore not a weakness but a necessary mechanism by which the discipline advances. The right response to any consensus on growth is not to defend it, but to ask what it cannot see.