Fiscal Convexity and Fiscal Anchors

A Note on Deficit Dynamics in Indonesia

This article does not take a position on specific policy choices but instead highlights how such choices may be interpreted and priced by markets, particularly within the context of emerging market fiscal dynamics. The views expressed are solely those of the author and do not reflect the views of any current, former, or prospective employer or affiliated institution.

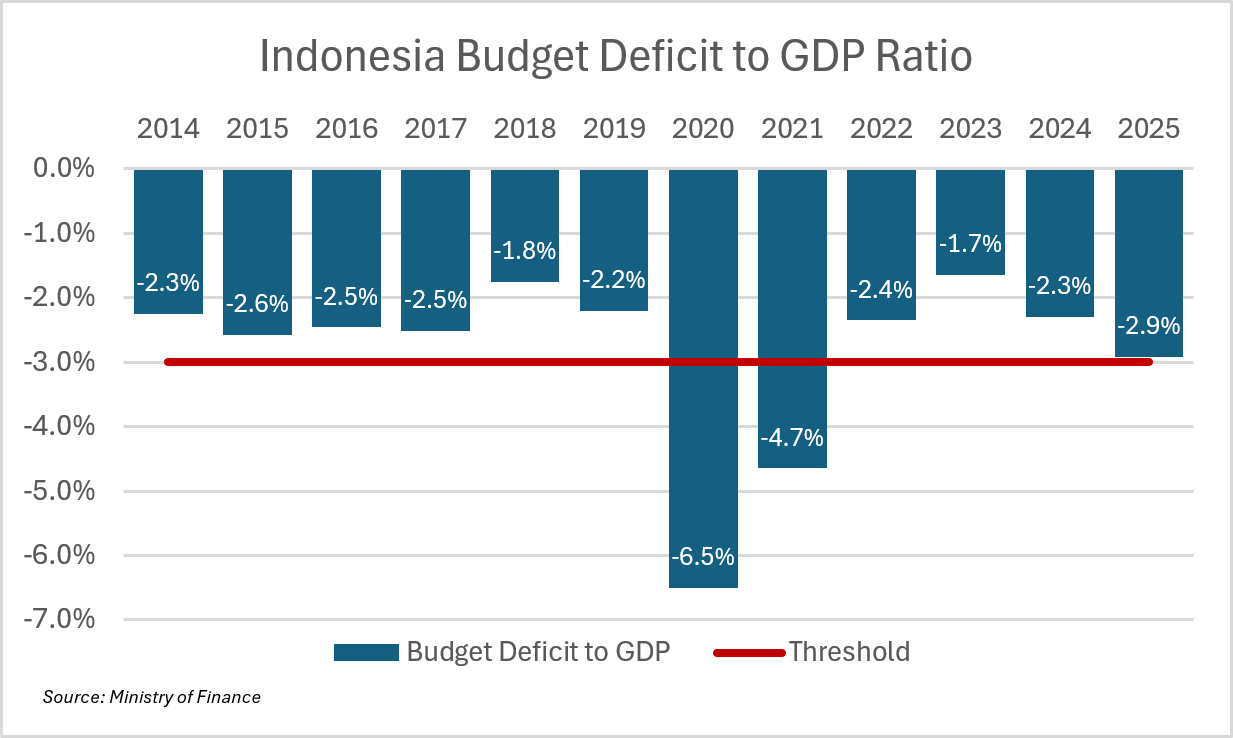

For more than two decades, Indonesia has operated under what is, in effect, a fiscal constitution: a deficit ceiling of 3% of GDP, codified in Law No. 17/2003. I didn’t live through the 1998 crisis that gave birth to this rule. But the data and institutional memory it left behind make its purpose clear. The Rupiah collapsed, private and state-owned banks failed and were forced into painful consolidation. The 3% rule was not designed as a technical guideline, it was a commitment, a signal to both domestic and global markets that Indonesia would not return to that kind of instability.

Source: Ministry of Finance via Trading Economics

In that sense, it functions less like a constraint and more like a pact. That pact has only been broken twice, in 2020 and 2021, under the extraordinary conditions of the pandemic, when fiscal rules around the world were temporarily suspended to prevent economic collapse. But what we are seeing now is different. The current discussion reflects pressures that appear more structural than cyclical. The government faces a growing set of spending commitments from large-scale social programs to infrastructure ambitions while also dealing with rising energy subsidy burdens driven by the conflict in the Middle East.

Within this context, the 3% ceiling is increasingly seen as a limitation rather than a safeguard. The argument for relaxing it is straightforward, and politically compelling. If additional spending can finance “productive” programs such as human capital development, housing, and institutional expansion, why should a rule drafted more than two decades ago stand in the way? At a glance, the constraint can feel arbitrary, even self-imposed.

But in emerging markets, numbers like this are rarely just numbers. They are reputational anchors. For investors, both domestic and foreign, the 3% threshold has long served as a simple, credible signal of fiscal discipline. It is part of the reason Indonesia has maintained investment-grade status and navigated episodes like the 2008 GFC and the 2013 Taper Tantrum without losing macroeconomic stability. This is where the tension becomes real. On one side, there is the promise of higher growth through expanded state spending. On the other, there is the risk of weakening the very anchor that has underpinned Indonesia’s credibility for over 20 years.

The question is not just whether we can afford to spend more. It is whether we can afford the cost of being perceived as less disciplined. Reading through the current discourse, I was reminded of Aizenman and Hausmann (1994), which offers a useful way to think about this. The key insight is simple but often overlooked: markets do not respond to fiscal changes linearly. A shift from a 3.0% to say, a 3.2% deficit may look trivial in arithmetic terms, just 0.2 percentage points. But in practice, such a move can trigger a disproportionately large reaction in sovereign risk. The reason lies in the convex nature of fiscal costs. As a country moves closer to, or appears to cross, a credibility threshold, the market response can accelerate sharply. What looks like a marginal deviation on paper can, in reality, be interpreted as a regime shift.

The Nonlinearity of Risk.

Fiscal dynamics in emerging markets are not linear. Standard models often assume a smooth relationship between debt and borrowing costs. In practice, that relationship bends. The cost of borrowing, captured by the sovereign risk premium, behaves convexly. As deficits rise toward a perceived threshold, the marginal cost of financing them does not increase gradually. It accelerates. Formally, if we think of borrowing costs as a function of the deficit C(d) then C”(d) > 0. The intuition is straightforward. Markets tolerate fiscal expansion up to a point. Beyond that point, tolerance turns into repricing.

As long as Indonesia stays within the 3% ceiling, it operates on the flat part of this curve. Small changes in the deficit have relatively small effects on borrowing costs. But once that anchor is questioned, even a modest increase can push the country toward the steep part of the curve, where perceptions of sustainability shift quickly. What appears incremental in fiscal terms can become discontinuous in market terms.

Asymmetric Risk and the Possibility of a Sudden Stop

This convexity creates an asymmetric payoff. On the upside, a marginal increase in the deficit may generate a modest boost to growth through the fiscal multiplier. The gains are real, but typically linear and gradual. On the downside, the same increase can be interpreted as a weakening of institutional discipline. If that happens, the adjustment is not gradual. Yields rise, the currency comes under pressure, and capital flows reverse. What follows is not a slowdown, but a repricing. This is the core insight in the Aizenman-Hausmann framework.

Fiscal rules in emerging markets act as hard signals that reduce information asymmetry. They allow investors to distinguish between deliberate policy and fiscal drift. Once that signal is weakened, the distinction becomes blurred. Investors respond defensively, pricing in the risk that discipline is no longer binding. The result can be a precautionary pullback in capital, often described as a sudden stop, where financing conditions tighten enough to offset the original stimulus.

When More Borrowing Reduces Fiscal Space

This dynamic leads to a counterintuitive result. Expanding the deficit does not always expand fiscal space. Abstracting from other complexities, government spending can be written as:

where G is spending, T is revenue (tax, non-tax, etc), and d is fiscal deficit. However, this identity hides an important channel, borrowing is not costless. The interest rate at which the government finances its deficit depends on how markets perceive fiscal risk. To capture this, let the interest rate be a function of the deficit, r(d), and let’s say that B denotes the existing stock debt. The marginal effect of increasing the deficit can therefore be written as:

The first term reflects the direct benefit of additional borrowing. The second term captures the increase in interest payments due to higher perceived risk. When the sensitivity of interest rates to deficits is low, additional borrowing increases fiscal capacity. But once credibility is in question and (dr/dd) rises, the opposite can happen. Each additional unit of debt raises borrowing costs on the existing stock. At that point, new borrowing is no longer financing spending. It is financing higher interest payments. That is the essence of a fiscal trap.

Conclusion: The Constraint That Protects

The temptation to breach the 3% deficit limit is understandable. In a developing economy with real infrastructure gaps and social needs, a rigid fiscal rule can feel outdated, even restrictive. But the cost of relaxing it is not just an additional 0.2% of GDP. It is a shift in how Indonesia is perceived.

Once the 3% cap is treated as a flexible guideline rather than a binding commitment, the signal it provides begins to weaken. And when that signal weakens, markets do not adjust gradually. They reprice risk. Higher yields, currency pressure, and tighter financing conditions can quickly offset any short-term gains from additional spending. What begins as an attempt to expand fiscal space can end up compressing it.

The Alternative: Expanding Capacity Without Expanding Risk

The case for productive spending is valid, but it does not require abandoning the anchor. It requires strengthening what sits behind it. This is something I keep coming back to after 2.5 years of working in fiscal policy, even if it sounds very repetitive. It has been said many times before, but that does not make it any less true. If anything, it reinforces the point: a more credibility-preserving approach is to remain within the existing framework:

1. Revenue Mobilization: Indonesia’s tax-to-GDP ratio remains structurally low. Expanding fiscal capacity through better compliance, administrative reform, and digitalization is slower than borrowing, but it does not carry the same credibility cost.

2. Allocative Efficiency: The binding constraint is not only how much is spent, but how effectively it is deployed. Reallocating broad, untargeted subsidies toward investments with higher multipliers, particularly in human capital and infrastructure, can deliver growth without destabilizing expectations.

Final Word

The 3% rule is not an arbitrary ceiling. It is a commitment that has anchored Indonesia’s fiscal credibility for over two decades. Relaxing it may create room in the short term. But it also changes the terms on which that room is financed. The real challenge is not how to move beyond the constraint, but how to operate more effectively within it.

References

Aizenman, J. and Hausmann, R. (2000) ‘The impact of inflation on budgetary discipline’, Journal of Development Economics, 63(2), pp. 425–449. doi:10.1016/s0304-3878(00)00111-5.