Cash Transfers and the Wrong Question

Cash, Credit, and the Unseen Effects of Social Protection: The Indonesia’s BLT/BLSM debate

Governments in developing countries frequently use unconditional cash transfers (UCTs) to shield households from adverse economic shocks. At their core, these programmes embody a simple idea: rather than prescribing what poor households need, the state gives them the means to decide for themselves.

These programmes are typically directed towards poor and vulnerable families. For a household confronting rising food prices, an unexpected illness, or a sudden loss of income, that flexibility can mean buying rice, paying for transport, keeping a child in school, covering medicine, meeting rent, or settling an urgent debt.

Indonesia has repeatedly relied on this policy instrument. Bantuan Langsung Tunai (BLT) was introduced in 2005, followed by Bantuan Langsung Sementara Masyarakat (BLSM) in 2013–14. Both programmes were introduced alongside politically difficult fuel-subsidy reforms, helping cushion poorer households from the resulting increase in living costs.

Yet the very flexibility that makes cash transfers appealing also makes them politically contested. When governments hand over cash with few conditions attached, a persistent question follows: what does a cash transfer really buy?

Cash transfers have long carried a moral anxiety. If recipients receive income without working, will they withdraw from the labour market? If they are free to spend the money as they choose, will it disappear into cigarettes, alcohol, or other so-called temptation goods? Beneath these questions lies a broader unease: that welfare may relieve hardship in the short term while quietly weakening self-reliance in the long term.

The empirical record, however, is far less dramatic than the political rhetoric. A growing body of evidence finds little support for the claim that cash transfers systematically reduce labour supply. Reviews of transfer programmes similarly find no average increase in spending on temptation goods. This does not mean that poor households always make perfect choices. Rather, it suggests that poverty is rarely a problem of insufficient discipline. More often, it is a problem of insufficient buffers: too little cash, too little security, and too little room to absorb a shock without falling further behind.

Indonesia provides an especially useful case. In a 2023 study, Ridho Al Izzati, Daniel Suryadarma, and Asep Suryahadi examined the behavioural effects of BLT and BLSM using longitudinal household data with a difference-in-difference design. Their result was straightforward: the transfers did not significantly alter employment, working hours, smoking, arisan participation, risk preferences, or patience.

These findings are reassuring. They weaken the familiar claim that cash transfers erode work ethic or invite irresponsible spending. But they do not show that transfers leave household economic behaviour unchanged. They simply suggest that the most visible forms of behavioural distortion may not be where the important adjustment occurs.

Cash transfers need not change people’s preferences to change the choices available to them. For households with little savings, unstable income, and limited access to formal insurance, even a modest transfer can alter the way a family manages risk. The relevant margin may not be whether a person works less or spends more on temptation goods. It may be whether the household borrows, from whom, and under what terms.

Borrowing is inherently ambiguous. It can be a lifeline: financing food after an income shock, covering medical treatment, keeping a small business operating, or preventing a child from leaving school. But it can also become a liability, creating repayment obligations that outlast the shock that first made the loan necessary.

This is where standard evaluations of cash transfers often remain incomplete. A transfer may substitute for debt by covering an urgent expense that would otherwise require borrowing. Yet it may also facilitate borrowing. A small cash buffer can help a household meet an upfront cost, approach a lender with greater confidence, or pursue an opportunity that previously appeared too risky.

More borrowing, then, is not automatically evidence of policy failure. Nor is less borrowing automatically evidence of success. The more difficult questions are who borrows, from whom, for what purpose, and at what cost.

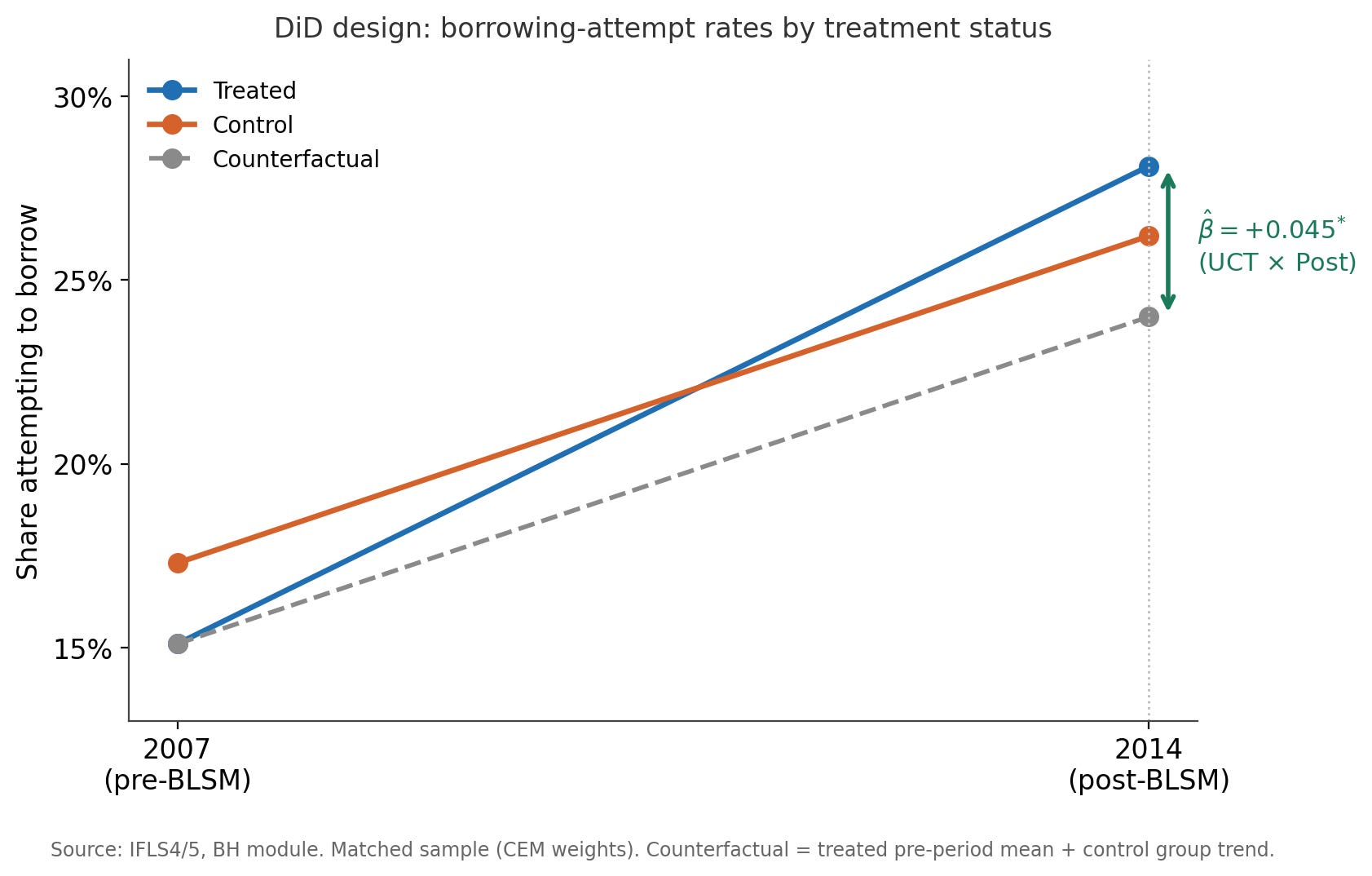

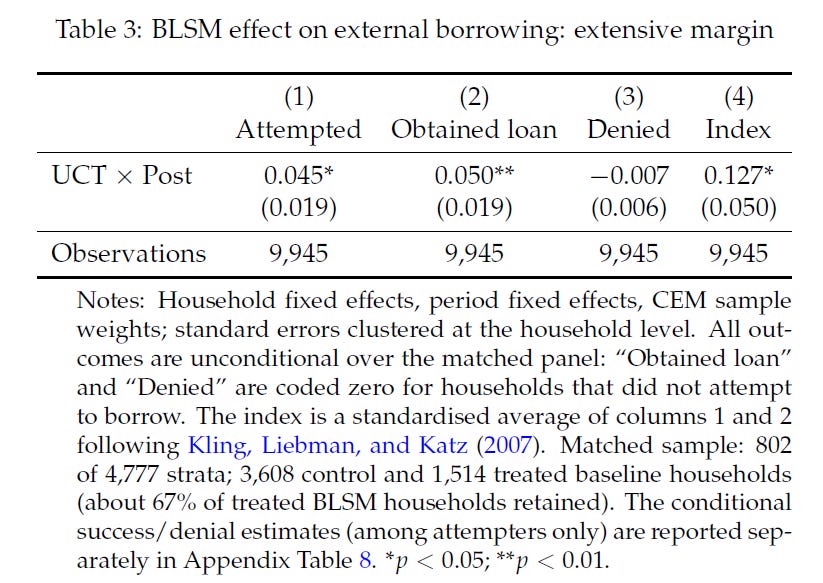

This was the question I explored in a replication and extension of Al Izzati, Suryadarma, and Suryahadi’s study of Indonesia’s Bantuan Langsung Sementara Masyarakat programme. I extended their analysis to external borrowing: loans obtained from sources other than family and friends.1

The result was counterintuitive. BLSM receipt actually increased the probability that a household attempted to borrow externally by 4.5 percentage points and obtained a loan by 5.0 percentage points. The pattern points less to an approval effect than to an entry effect. BLSM did not appear to make lenders more willing to approve applications; rather, it was associated with more households entering the external credit market in the first place.

The future of cash transfers should not be framed as a choice between blind optimism and moral panic. Unconditional transfers remain valuable when households need immediate relief and flexibility. Conditional transfers, therefore, may be appropriate when governments seek particular investments in education, health, or nutrition. But neither should be assessed only through consumption or labour-market outcomes.

A serious evaluation of social protection should also ask whether households borrow, what kind of credit they use, what that credit costs, and whether it helps them recover from a shock or merely postpones hardship.

Cash transfers may not change who people are. But they can change the financial constraints under which people make decisions. That, too, is a behavioural effect worth taking seriously.